Fun Ifrs 16 In Cash Flow Statement Dell Financial Ratios

Ifrs 16 Leases Ifrs 16 Leases The 3 Trillion Standard One Of My Great Ambitions Before I Die Is To Fly In An Aircraft That Is On An Airline S Balance Ppt Download

Statement of financial position consolidated cash flow statement and the notes relevant to IFRS 16 and that are affected by the initial application of IFRS 16 are included. IFRS 16 sets out a comprehensive model for the identification of lease arrangements and their treatment in the financial statements of both lessees and lessors. IFRS 16 requires most leases to be recorded on balance sheet and therefore cash outflows arising from financing activities will generally increase due to IFRS 16. Both operating cash flow as a component of enterprise free cash flow and net debt are key components in an enterprise value based DCF analysis. In January 2016 IAS 7 was amended by Disclosure Initiative Amendments to IAS. Many entities under IAS 17 classified cash outflows associated with operating leases as operating cash flows meaning that the adoption of IFRS 16 results in a reduction in amounts classified as operating cash outflows and a corresponding increase in amounts classified as financing cash outflows. Initial direct costs paid in. In contrast IFRS 16 includes specific requirements for the presentation of the ROU asset and lease liability and the corresponding effects on the results and cash flows in the primary financial statements. The underlying lessee accounting model has changed and this together with the explicit requirements in the standard see In technical speak below mean that entities need to reconsider the classification of lease payments. With net assets unchanged this may seem innocuous but it is the calculations that are derived from balance sheet figures for working capital liquidity and perceived borrowings Financing Loans where the problems can arise as follows.

The standard requires the lessee to recognise assets and liabilities for all leases with more than 12 months tenor unless the underlying asset is.

Both operating cash flow as a component of enterprise free cash flow and net debt are key components in an enterprise value based DCF analysis. 211 Statement of financial position. The present value of the lease liability is CU 17 000. The underlying lessee accounting model has changed and this together with the explicit requirements in the standard see In technical speak below mean that entities need to reconsider the classification of lease payments. As operating type ie. The objective of IFRS 16 is to faithfully represent lease-based transactions and support users assessment of cash flows arising from leases.

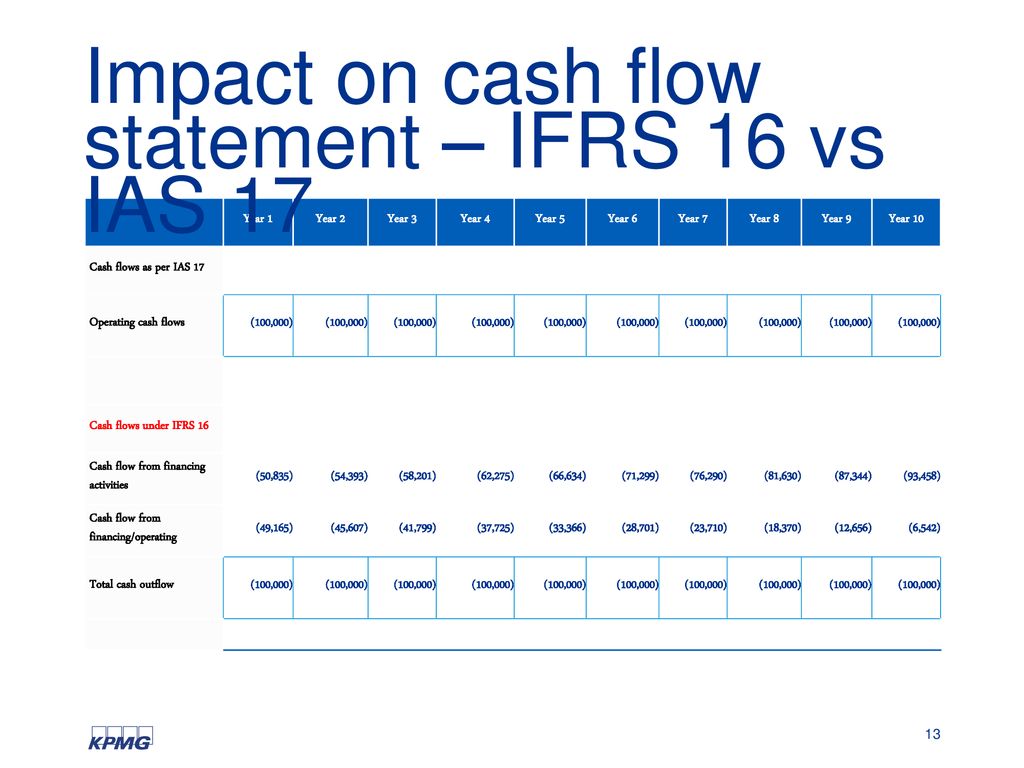

The problem is that under IFRS 16 cash flows are reclassified which impacts the measurement of operating cash flow and new debt appears on the balance sheet. Statement of cash flows Leases impact the statement of cash flows in the following way IFRS 1650. The objective of IFRS 16 is to faithfully represent lease-based transactions and support users assessment of cash flows arising from leases. Cash Flow and Financing. Repayments of the principal portion of the lease liability are presented within financing activities payments relating to accrued interest are classified according to. 211 Statement of financial position. Initial direct costs paid in. There may however be a change in how cash flows appear in the cash flow statement. IFRS 1653 Relating to the statement of cash flows Total cash outflow for leases IFRS 1655 Other Amount of short-term lease commitments if current short-term lease expense is not representative for the following year IFRS 1658 60 Qualitative disclosures Description of how liquidity risk related to lease liabilities is managed. With net assets unchanged this may seem innocuous but it is the calculations that are derived from balance sheet figures for working capital liquidity and perceived borrowings Financing Loans where the problems can arise as follows.

Financial Statements and IAS 7 Statement of Cash Flows. In contrast IFRS 16 includes specific requirements for the presentation of the ROU asset and lease liability and the corresponding effects on the results and cash flows in the primary financial statements. As a result of the changes in terminology used throughout the IFRS Standards arising from requirements in IAS 1 Presentation of Financial Statements issued in 2007 the title of IAS 7 was changed to Statement of Cash Flows. This is because the op cash flow will increase the financing cash flow will decrease by same amount. Off balance sheet from the perspective of lessees with their respective cash flows included in operating activities. The problem is that under IFRS 16 cash flows are reclassified which impacts the measurement of operating cash flow and new debt appears on the balance sheet. IFRS 16 is likely to have a significant impact on the financial statements of a number of lessees. The standard requires the lessee to recognise assets and liabilities for all leases with more than 12 months tenor unless the underlying asset is. IFRS 16 applies a control model for the identification of leases distinguishing between leases and service contracts on. Follow IFRS 16 classification and treat lease payments as cash flows to debt providers in the discounted cash flow model and subtract the fair value the lease liability from the outcome as applicable.

IFRS 1653 Relating to the statement of cash flows Total cash outflow for leases IFRS 1655 Other Amount of short-term lease commitments if current short-term lease expense is not representative for the following year IFRS 1658 60 Qualitative disclosures Description of how liquidity risk related to lease liabilities is managed. Follow IAS 17 cash flow classification and continue modelling the cash flows as before treating the lease. In contrast IFRS 16 includes specific requirements for the presentation of the ROU asset and lease liability and the corresponding effects on the results and cash flows in the primary financial statements. As operating type ie. Statement of cash flows Leases impact the statement of cash flows in the following way IFRS 1650. In January 2016 IAS 7 was amended by Disclosure Initiative Amendments to IAS. What is IFRS 16. The underlying lessee accounting model has changed and this together with the explicit requirements in the standard see In technical speak below mean that entities need to reconsider the classification of lease payments. The standard requires the lessee to recognise assets and liabilities for all leases with more than 12 months tenor unless the underlying asset is. IFRS 16 sets out a comprehensive model for the identification of lease arrangements and their treatment in the financial statements of both lessees and lessors.

Statement of cash flows Leases impact the statement of cash flows in the following way IFRS 1650. Note 13 Income taxes Note 16 Earnings per share and. Follow IAS 17 cash flow classification and continue modelling the cash flows as before treating the lease. In January 2016 IAS 7 was amended by Disclosure Initiative Amendments to IAS. Statement of financial position consolidated cash flow statement and the notes relevant to IFRS 16 and that are affected by the initial application of IFRS 16 are included. Initial direct costs paid in. IFRS 16 is likely to have a significant impact on the financial statements of a number of lessees. IFRS 16 Leases in the statement of cash flows IAS 7 On 1 January 20X4 ABC entered into the lease contract. This is because the op cash flow will increase the financing cash flow will decrease by same amount. Cash Flow and Financing.

The objective of IFRS 16 is to faithfully represent lease-based transactions and support users assessment of cash flows arising from leases. The details are as follows. A discussion of the impact of IFRS 16 on the statement of cash flows is included in Section 13. Note 13 Income taxes Note 16 Earnings per share and. Statement of cash flows Leases impact the statement of cash flows in the following way IFRS 1650. In January 2016 IAS 7 was amended by Disclosure Initiative Amendments to IAS. Under IFRS 16 a contract is or contains a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. IFRS 1653 Relating to the statement of cash flows Total cash outflow for leases IFRS 1655 Other Amount of short-term lease commitments if current short-term lease expense is not representative for the following year IFRS 1658 60 Qualitative disclosures Description of how liquidity risk related to lease liabilities is managed. Financial Statements and IAS 7 Statement of Cash Flows. Initial direct costs paid in.